It started life behind the Iron Curtain – now UK-listed Avast could become the latest to succumb to a US takeover

Another day and another leading UK company is in talks to be taken over.

This time, it is Avast, the cyber security provider and one of the biggest tech companies listed on the London Stock Exchange.

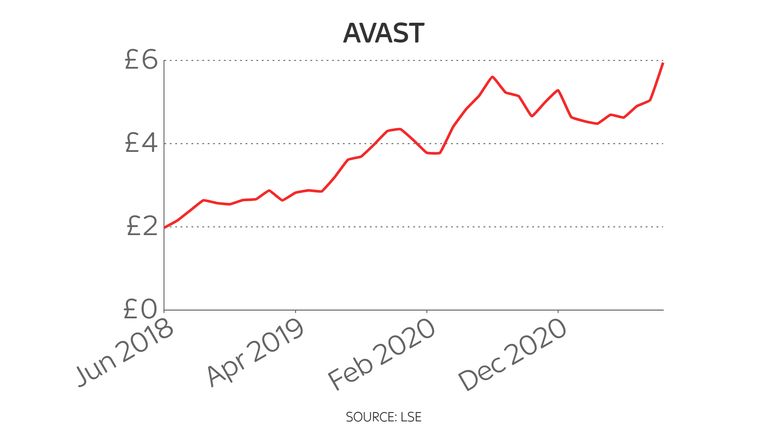

Avast, which floated on the stock market in May 2018 and which was promoted to the FTSE 100 in June last year, confirmed overnight it is in “advanced” talks to sell itself to its US rival Norton LifeLock.

Avast’s share price has more than doubled since its flotation

Shares of the company, which have doubled in value since the flotation, have surged by 13% on the news.

Avast, whose stock market valuation at the close on Wednesday evening was £5.2bn, is expected to be taken out at a value close to £5.9bn.

That would represent a decent premium to the price at which the shares have changed hands during the last five months or so but would nonetheless still represent a modest discount to the price at which they were trading in July and August last year.

A deal, on top of swoops for UK-listed companies such as John Laing, St Modwen, Signature Aviation, Spire Healthcare, Aggreko and the recent deal agreed for Morrisons, is sure to provoke more anguished discussion.

There is a growing sense among some politicians and some in the media, as well as in fund management circles, that the boards of many UK-listed companies are agreeing too readily to takeovers by foreign buyers and, in particular, to takeovers by private equity firms.

It may be harder to build such a sense of outrage in the case of Avast, however, since it is not exactly a company that is draped in the Union Jack.

Avast and Norton have strong positions in the consumer market

The company’s global headquarters is in Prague, where the vast majority of its 1,700 employees worldwide are based, with just 100 or so in the UK.

Nonetheless, Avast’s decision to list not in New York but in London was a welcome boost to the latter’s tech credentials, while its takeover would reduce the ranks of “pure” tech companies in the FTSE to just two – the engineering software group Aveva and the accounting software group Sage.

It would also deprive the UK market of what has been an inspiring story.

Avast emerged from a workers co-operative called ALWIL which was founded in then-Communist Czechoslovakia in 1988 a year before the fall of the Berlin Wall.

After the collapse of Communism, the co-operative’s founders, computer scientists Eduard Kucera and Pavel Baudis, set it up as a company, having already made their names defeating a computer virus called the Vienna bug.

The business had to fend off unwanted takeover approaches from rivals such as McAfee and at one point came close to collapse after struggling to conquer the United States.

The company’s fortunes turned around when, in 2001, it adopted a freemium business model, making the most basic version of its anti-virus software free to download, but charging for premium services and selling corporate licences.

Less than three years later, its software had been downloaded by more than one million people.

Avast chose London rather than New York when it floated in 2018

It now boasts an estimated 435 million users around the world and more than 13 million of them are paying customers.

The company was a beneficiary of the pandemic, putting on more than one million such paying customers during 2020, partly because of a rise in demand from people working from home and seeking extra security for their phone or telephone.

It is also a business that values continuity in more ways than one: the current chief executive, Ondrej Vlcek, joined the business as an 18-year old intern more than 25 years ago and has remained there ever since.

A takeover is not yet a done deal.

While there has been an increase in competition in the cyber security sector in recent years, with Microsoft in particular taking market share, competition regulators around the world may take a dim view of two such well-known players in the anti-virus space getting together and particularly as both have strong positions in the consumer market.

Some investors may also demand more of a premium: analysts at Berenberg bank told clients this morning that “nothing short of a $10bn (£7.2bn) valuation is fair to Avast’s shareholders”.

That may ultimately come down to Mr Baudis and Mr Kucera who, respectively, have 25% and 10% stakes in the business.

Mr Vlcek owns a further 2.3% stake.

Avast adopted a freemium business model in 2001 Pic:Avast

Norton’s approach is also likely to spark interest from private equity companies.

Avast could probably live with such an ownership structure as it has experience of it.

When it came to market it was 23% owned by CVC Capital Partners.

But management would be justified in pushing for a higher price.

Avast is already growing strongly in a lot of markets around the world.

Mr Vlcek noted in March, at the company’s results presentation, that it had, in the previous 12 months, enjoyed a 33% rise in customers in Mexico, 19% growth in Brazil, 17% growth in Argentina and 16% growth in Ukraine.

That growth is only going to accelerate as the ‘Internet of Things’ (IoT) takes off and everyday items like fridges and cookers become potentially more susceptible to hacking attacks.

Avast may not be one of the best-known companies in the FTSE 100.

But it will be missed if it is taken over.