Markets fret as consumers and investors lose faith in central banks keeping a lid on inflation

The price of natural gas is soaring – and both equity and bond markets are again fretting about surging inflation.

The cost of wholesale gas for next-day delivery in the UK today hit an all-time high of £3.55 per therm (one therm is equal to 100 cubic feet of natural gas), a rise of 27%, meaning the price has doubled in a week.

The immediate upshot is that more “challenger” household energy suppliers, who tend to buy their gas on the spot market rather than in advance, are likely to topple over.

Energy boss: It’s ‘crunch time’ for many small providers

This is not just an issue in the UK.

Natural gas prices are rising across Europe due to a combination of liquefied natural gas cargoes being diverted to Asia to meet growing demand there, lower supplies from Russia and lower output from renewable energy sources such as wind and solar.

The United States is also seeing a surge in natural gas prices.

Stock markets have suffered several bouts of unease this year amid signs that inflation is taking off.

There was a notable sell-off early in May reflecting a rise in the price of commodities such as copper and the cost of shipping, exacerbated in March by the stranding in the Suez Canal of Ever Given, a container ship en route from China.

On that occasion, markets took at face value the insistence of central bankers such as Jay Powell at the US Federal Reserve, Christine Lagarde at the European Central Bank and Andrew Bailey at the Bank of England that the inflation starting to appear was simply “transitory”, a reflection of surging demand as economies re-opened after the pandemic.

The standing of the Ever Given in the Suez Canal exacerbated factors behind a sell-off earlier this year

Investors around the world are now taking the threat more seriously.

For example, in Japan, the world’s fourth largest energy importer, the Nikkei 225 has fallen in each of the last eight sessions, taking it into correction territory.

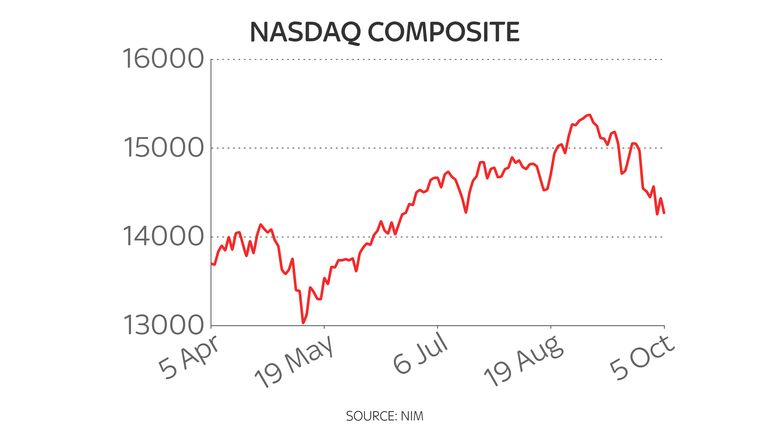

Similarly, the Dax in Germany is down to a level last seen in May, while the Nasdaq – which is full of tech stocks which tend to move in close correlation to expected movements in interest rates – fell this week to a level last seen in June.

The anxiety about inflation is playing out most markedly in the sovereign debt markets.

The yield on 10-year UK government gilts (the yield on a bond rises as the price falls) has surged from 0.621% at the start of September to 1.15% – a level not seen since May 2019 – today.

In the same period, the yield on 10-year US Treasuries has risen from 1.307% to 1.552%, while yields on Treasuries of other durations have also risen.

Several things have changed since May.

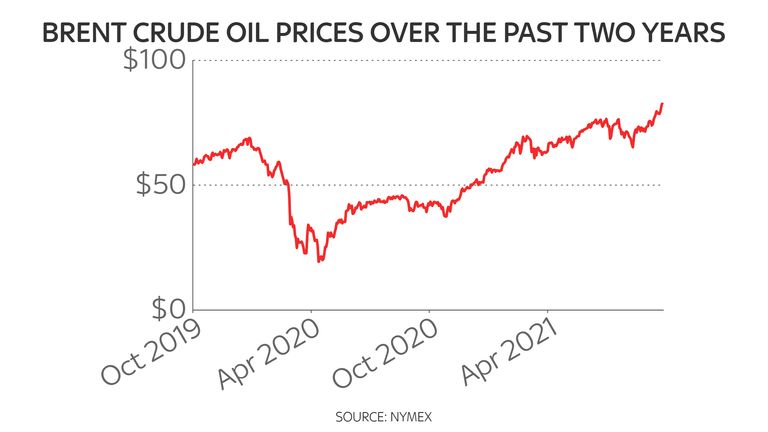

The first and most obvious is that the price of crude oil has continued to grind higher.

The Nasdaq has fallen to levels last seen in June

In May, during the last inflation-inspired stock market squalls, a barrel of Brent Crude traded at between $64-$70 a barrel.

This month, so far, it has traded in a range between $77-$83 a barrel.

The main US oil contract, West Texas Intermediate, has seen an even sharper move higher and is now trading at a level last seen in November 2014.

That is starting to feed into inflation expectations – something central bankers everywhere watch warily because it usually tends to feed into higher wage demands.

For example, two weeks ago, the latest survey of inflation expectations carried out by the investment bank Citi and the pollsters YouGov found that the British public is expecting inflation to hit 4.1% over the next year.

It is a similar picture elsewhere.

The latest survey from the University of Michigan, which is closely watched by US policymakers, this week pointed to rising inflation expectations among American consumers.

And a market measurement of inflation expectations among consumers in the eurozone – a part of the world that during the last decade has had to worry more about deflation, or falling prices, than inflation – this week hit its highest level for six years.

The price of crude oil has continued to grind higher

In other words, consumers and investors in the US, the UK and the eurozone appear to be losing faith in the ability of their central banks to keep a lid on the cost of living.

That belief is entirely rational if, for example, you are a British motorist who has spent hours during the last couple of weeks trying to find petrol or, for example, you are an American consumer looking at big increases in the price of your weekly grocery shop.

What is particularly interesting is that a number of so-called “trimmed mean” inflation measures, which strip out the more extreme price changes of items in the inflationary “basket”, suggest the headline rate of inflation in the US is being artificially depressed by big drops in items such as air fares and hotel rooms.

They imply that underlying inflation – that element of inflation that cannot simply be explained away by pandemic-influenced levels of supply and demand – is actually much higher.

The third factor is that some investors are now starting to think seriously about “stagflation” – the ghastly combination of stagnant growth and inflation last seen in the 1970s.

Google searches for the term “stagflation” have in the last week hit their highest level since July 2008, when the global financial crisis was getting under way.

Now, there are several good reasons to argue that we are not in for a re-run of the 1970s, not least the fact that the world is less dependent on oil than it was then and the fact that the trades unions – in Britain at least – are not as powerful as they were then.

But such searches do point to a change of sentiment among not only investors but the wider public.

British motorists have spent hours stuck in petrol queues

There is every reason to think that inflation may well rise in coming weeks and months.

A clutch of UK companies, including the car and aerospace parts supplier Melrose, the bakery chain Greggs, the furniture and floorcoverings retailer ScS and the online fashion retailer Boohoo have all in the last week highlighted labour shortages, supply chain issues and rising input costs.

And that is likely to feed into higher bills for consumers.

Petrol prices are already at their highest level for eight years.

The increase in the energy price cap this week will result in higher household energy bills for 15 million UK households.

And recent rises in the price of a number of agricultural commodities in recent weeks mean that food price increases are looming.

Further eating away at the ability of consumers to spend will be next year’s increases in national insurance.

In London, meanwhile, nearly 350,000 households and businesses are about to fall foul of Mayor Sadiq Khan’s extension of his ultra low emissions zone, obliging them to either replace their vehicle at vast expense or pay a £12.50 daily fine – again carrying the same effect as inflation.

In short, there are a lot of reasons why consumers and businesses alike have good reason to believe that current levels of inflation are not just transitory, but more deep-seated.

The Bank of England – along with its counterparts around the world – has its work cut out to persuade them otherwise.