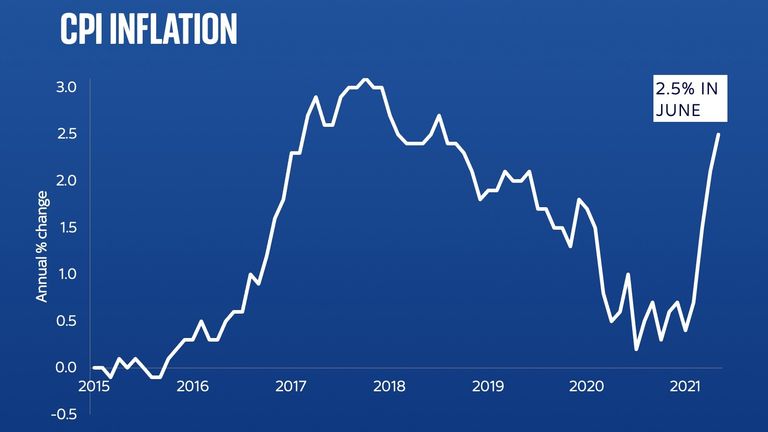

Signs that inflation rise is temporary – but could it prove sticky?

There are, in very broad terms, two schools of thought about the recent rise in inflation.

The first is that while prices are certainly accelerating faster than expected (this is the second month in which the consumer price index (CPI) rate of inflation was both above the Bank of England’s 2% target and higher than economists expected) this pressure will soon abate. That, generally, is the Bank’s view.

And indeed, while CPI inflation rose to 2.5% in June, and is expected to rise above 3% later on this year, there are perhaps one or two signs, when you dig down into the figures themselves, that this might be temporary.

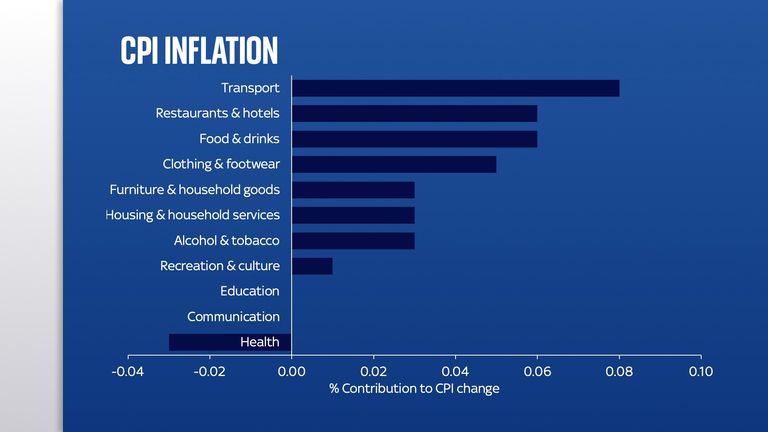

For alongside the inflation data – essentially a measure of the average price of a typical “shopping basket” of goods and services – we get data on the prices companies pay for their raw materials.

These “input prices” have been going up very sharply in recent months – especially for certain goods associated with construction: stuff like timber, cement and metals. While those prices are still rising very fast, the rate may now have peaked.

In June, for instance, the annual price increase (in other words inflation rate) of cement and concrete dropped from 18% to 16.9%. Iron, steel and basic metals price inflation also dropped somewhat. Fish price inflation – which may have been pushed up by issues surrounding the end of the Brexit transition – dropped from 35.4% in May to 11.3% in June.

Now, note these prices are still going up rapidly – albeit less rapidly than before. But it is perhaps the first sign that the pipeline of price pressure is starting to abate.

Overall, input prices – the costs producers pay for their raw materials – dropped from 10.4% to 9.1%. This might not smack of deflation or disinflation, but it’s nonetheless a reminder that prices may not keep going up at the current rapid rate forever.

However, the other school of thought is that even if these input prices abate, there is a serious risk that inflation could prove “sticky”.

In other words that having seen prices climb higher, workers demand higher wages which causes a “spiral” in both wages and then prices.

That’s something that’s happened in the past, though not for some decades. It is a phenomenon that haunts economic policymaking.

Let’s not forget that the very reason the Bank has an inflation target is to guard against the high inflation that afflicted the UK and many other countries in the 1970s and ’80s.

All of which is to say the coming months will be nervy ones, both for the Bank of England and the rest of us.

Interest rates – the Bank’s main tool to control the economy – are at the lowest level in history, yet the Bank does not seem inclined to raise them, or curtail its quantitative easing programme (as it typically would to combat high inflation) any time soon.